Posted on

01/07/205

Home Appraisals: Your Essential Guide for 2025

The home appraisal protects buyers and lenders from overpaying for a property. Most U.S. homeowners lack proper insurance coverage, making accurate property valuation crucial for protecting their investments.

Home appraisals typically cost $300 to $450, with prices reaching $700 in high-demand markets like California. The appraiser needs 30 minutes to several hours at your property, while the process takes about a week to complete. When appraisals come in below expected value, you'll

need to either renegotiate the price, make up the difference in cash, or walk away from the deal.

This guide walks you through the appraisal process step by step. You'll learn what happens during a property inspection, what drives the cost, and how to prepare your home. We explain the key factors affecting your property's value and help you spot potential problems before they arise.

What Happens During a Home Appraisal

"The 2025 UAD overhaul introduces a flexible, customizable format for appraisals. Unlike the traditional, static forms, the new UAD 3.6 system tailors each report to match the property specifics, including only the necessary data fields." — Capital Valuations VA, Real Estate Valuation Company

Depending on the home's size and layout, the assigned appraiser views and measures your property during an on-site visit between 30 minutes and a few hours.

The Initial Property Walkthrough

The appraiser starts by walking through your entire home. They count bedrooms and bathrooms while assessing the floor plan's functionality. Both interior and exterior features are carefully examined to understand your home's essential characteristics.

Taking Measurements and Photos

The appraiser documents every aspect of your property. They take detailed photographs and create an exterior sketch of the building. The final report must include:

Maps showing the property location

Exterior photos - front and back views

Pictures of comparable properties used

Complete property layout documentation

Photos of each room

Checking Home Condition

The appraiser examines your home's key components. They assess the foundation, roof condition, walls, and structural elements.

During this inspection, they check all significant systems, such as HVAC and plumbing. Your home's features and recent improvements get special attention since these affect the final value. The appraiser notes any issues needing repair or safety concerns that might lower the property value.

The inspection goes beyond the main living spaces. The appraiser examines attics, basements, and crawl spaces to verify safety standards and assess their contribution to home value. Outside areas like landscaping, decks, and other improvements are also factors in the final assessment.

Home Appraisal Costs for 2025

The cost of the home appraisal is traditionally the buyer's responsibility. Most homeowners pay around $357, with the national average for a single-family home appraisal falling between $314 and $423.

What Affects the Cost

Square footage plays a significant role in your appraisal fee. Larger homes need more time to evaluate, which increases the cost. Properties in high-cost areas often start at $600.

Different loan types require different levels of detail. Here's what you'll pay for government-backed loans:

FHA appraisals: $400 to $700

VA appraisals: $425 to $900

Property condition and access also matter. Well-maintained homes with easy access stay within standard price ranges. However, homes with structural problems or hard-to-reach areas might cost over $1,000 for a basic assessment.

Market activity in your area affects pricing. The high demand for appraisers drives up costs. Rural properties and unique homes require more research time, leading to higher fees.

Key Factors That Impact Your Home's Value

"Homes with more usable space generally appraise higher, so any functional improvements or optimizations can be a plus." — Better Mortgage, Digital Mortgage Lender

The appraiser looks at several key elements when determining your property's worth. These factors work together to give us your home's actual market value.

Location and Neighborhood

Location remains the ever-popular "location, location, location" factor in property value. Homes near quality schools, shopping centers, and public transportation attract higher prices, and buyers are more interested in properties in safe neighborhoods with good school districts.

Future neighborhood prospects matter, too. New roads, shopping centers, and other developments boost property values, and job growth in the area often means rising home prices.

Property Size and Layout

Square footage tells part of the story. A 2,000-square-foot house selling for $200,000 is priced at $100 per square foot. But usable space matters more than raw numbers. We don't count garages, attics, or unfinished basements in the living space calculations.

The floor plan's function weighs heavily in our assessment. Homes get better valuations with:

Open layouts joining kitchen, dining, and living spaces

Multiple bedrooms and bathrooms

Natural light and good room flow

Recent Upgrades

Smart improvements add real value. A basic kitchen update that costs $27,492 brings back $26,406 at sale—96.1% returned. Practical fixes work better than complete overhauls.

Outside improvements pay off, too. A new front door costs $2,355 but returns 188.1% at sale. A garage door replacement, at $4,513, brings back 193.9%. Fresh paint typically adds $10,184 to home value.

Market Conditions

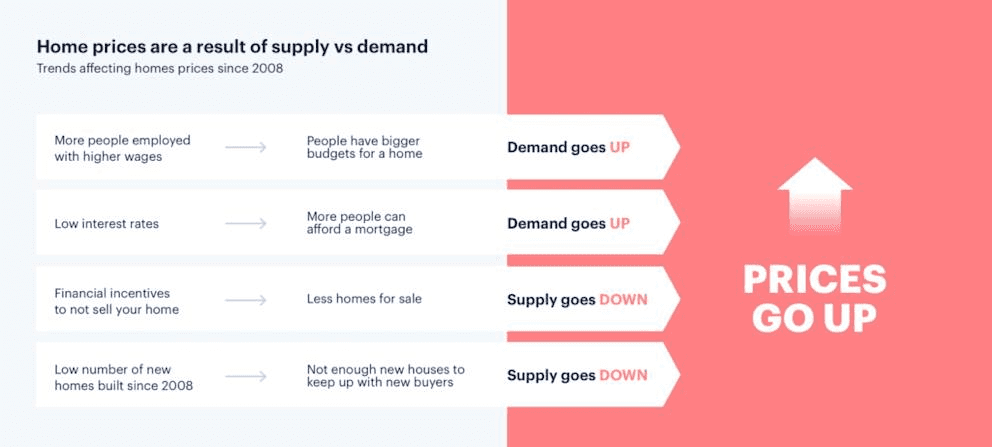

Supply and demand drive property values. When fewer homes are for sale, prices rise as buyers compete. Lower interest rates usually bring more buyers to the market.

The broader economy also affects home values. Harvard's research shows that Americans plan to spend $509 billion fixing up homes in 2025. Homeowner equity grew 2.5% in late 2024, indicating the market's health.

Common Home Appraisal Problems

The home appraisal process can encounter some obstacles. Here are some things to watch for and how to handle these common issues.

Low Appraisal Value

Buyers and sellers face tough decisions when appraisals come in below the agreed purchase price. The appraiser might have used old data or missed recent sales in your area.

Watch out if you're near foreclosures or bank-owned properties. These distressed sales can lower the neighborhood's values. Buyers in declining markets might need to make more significant home down payments.

Property Condition Issues

The appraiser must note any problems affecting your home's safety and structure. Properties rated C6 show serious difficulties and won't qualify for regular loans until they are fixed. They look for:

Foundation damage or structural issues

Old HVAC systems needing replacement

Broken windows or missing handrails

Signs of pest problems

Roof troubles needing certification

Don't get stuck holding the bag on repairs - foundation work runs from $4,000 to $100,000 for full replacement. Homes rated C1 through C4 can still get loans, but C5 and C6 properties need repairs first.

Missing Documentation

Suitable paperwork makes all the difference. The appraiser needs to see and measure every part of your property. Missing documents can stall the process or lower your value.

Tell the appraiser about your improvements - skipping this step often means a lower value. Show receipts and photos of your upgrades to support a higher number.

Think your appraisal missed the mark? You can ask for a Reconsideration of Value (ROV). But you'll need proof - either overlooked improvements or comparable sales the appraiser didn't see. Keep those renovation records handy to back up your home's worth.

How to Prepare for Your Home Appraisal

A well-prepared home shows the appraiser that you care about maintenance. Taking time to get ready makes a real difference in your final value.

Clean and Declutter

The appraiser sees a clean, organized home as a sign of good maintenance. Take out anything that makes rooms look smaller or blocks important areas. A thorough cleaning lets the appraiser see your home's condition without distractions.

Start with these spots:

Deep clean those carpet stains

Touch up paint where needed

Make sure we can get to attics and crawl spaces

Power wash the outside

Clean up the yard and landscaping

Gather Important Documents

The appraiser needs good records to value your property right. Create a detailed list of recent improvements with dates and costs. Pull together these papers after you schedule the appraisal:

Old appraisal reports

Property tax papers

Renovation permits

Recent home inspections

Records of major upgrades

Fix Minor Issues

Don't let minor problems hurt your value. The appraiser uses the "$500 rule" - valuing homes in $500 steps. Small repairs can add significant value when you fix several things.

Take care of these typical troubles:

Fix those leaky faucets

Patch damaged walls and paint

Replace broken door handles

Tighten loose handrails

Check all mechanical systems

Make sure safety equipment works, too. Test carbon monoxide detectors, smoke alarms, and garage door openers. Fixing these items shows you take care of the property.

The outside counts just as much. Trim those bushes, mow the lawn, and clear out dead plants. Add some flowers in warm months, or keep snow cleared in winter.

Tell the appraiser about neighborhood improvements, too. New schools, parks, or better roads can boost your property's value. Your local knowledge helps you get the most accurate number for your property.

Conclusion

The home appraisal protects both you and your lender. Understanding and preparing for the process can help you secure your property's actual value.

The property condition tells the story. Clean, well-kept homes with good improvement records bring better numbers. A little effort in fixing minor problems and organizing paperwork before the appraiser arrives makes a real difference.

Banks Valuation takes great pride in offering accurate, fair valuations based on current market conditions and neighborhood factors. We understand how location and market trends shape your property's worth.

Trust us to guide you through the appraisal process. We handle any issues quickly and communicate openly with all parties. Our team of expert appraisers delivers the attention to detail, proper preparation, and professional guidance your valuable investment deserves.

The home appraisal protects buyers and lenders from overpaying for a property. Most U.S. homeowners lack proper insurance coverage, making accurate property valuation crucial for protecting their investments.

Home appraisals typically cost $300 to $450, with prices reaching $700 in high-demand markets like California. The appraiser needs 30 minutes to several hours at your property, while the process takes about a week to complete. When appraisals come in below expected value, you'll

need to either renegotiate the price, make up the difference in cash, or walk away from the deal.

This guide walks you through the appraisal process step by step. You'll learn what happens during a property inspection, what drives the cost, and how to prepare your home. We explain the key factors affecting your property's value and help you spot potential problems before they arise.

What Happens During a Home Appraisal

"The 2025 UAD overhaul introduces a flexible, customizable format for appraisals. Unlike the traditional, static forms, the new UAD 3.6 system tailors each report to match the property specifics, including only the necessary data fields." — Capital Valuations VA, Real Estate Valuation Company

Depending on the home's size and layout, the assigned appraiser views and measures your property during an on-site visit between 30 minutes and a few hours.

The Initial Property Walkthrough

The appraiser starts by walking through your entire home. They count bedrooms and bathrooms while assessing the floor plan's functionality. Both interior and exterior features are carefully examined to understand your home's essential characteristics.

Taking Measurements and Photos

The appraiser documents every aspect of your property. They take detailed photographs and create an exterior sketch of the building. The final report must include:

Maps showing the property location

Exterior photos - front and back views

Pictures of comparable properties used

Complete property layout documentation

Photos of each room

Checking Home Condition

The appraiser examines your home's key components. They assess the foundation, roof condition, walls, and structural elements.

During this inspection, they check all significant systems, such as HVAC and plumbing. Your home's features and recent improvements get special attention since these affect the final value. The appraiser notes any issues needing repair or safety concerns that might lower the property value.

The inspection goes beyond the main living spaces. The appraiser examines attics, basements, and crawl spaces to verify safety standards and assess their contribution to home value. Outside areas like landscaping, decks, and other improvements are also factors in the final assessment.

Home Appraisal Costs for 2025

The cost of the home appraisal is traditionally the buyer's responsibility. Most homeowners pay around $357, with the national average for a single-family home appraisal falling between $314 and $423.

What Affects the Cost

Square footage plays a significant role in your appraisal fee. Larger homes need more time to evaluate, which increases the cost. Properties in high-cost areas often start at $600.

Different loan types require different levels of detail. Here's what you'll pay for government-backed loans:

FHA appraisals: $400 to $700

VA appraisals: $425 to $900

Property condition and access also matter. Well-maintained homes with easy access stay within standard price ranges. However, homes with structural problems or hard-to-reach areas might cost over $1,000 for a basic assessment.

Market activity in your area affects pricing. The high demand for appraisers drives up costs. Rural properties and unique homes require more research time, leading to higher fees.

Key Factors That Impact Your Home's Value

"Homes with more usable space generally appraise higher, so any functional improvements or optimizations can be a plus." — Better Mortgage, Digital Mortgage Lender

The appraiser looks at several key elements when determining your property's worth. These factors work together to give us your home's actual market value.

Location and Neighborhood

Location remains the ever-popular "location, location, location" factor in property value. Homes near quality schools, shopping centers, and public transportation attract higher prices, and buyers are more interested in properties in safe neighborhoods with good school districts.

Future neighborhood prospects matter, too. New roads, shopping centers, and other developments boost property values, and job growth in the area often means rising home prices.

Property Size and Layout

Square footage tells part of the story. A 2,000-square-foot house selling for $200,000 is priced at $100 per square foot. But usable space matters more than raw numbers. We don't count garages, attics, or unfinished basements in the living space calculations.

The floor plan's function weighs heavily in our assessment. Homes get better valuations with:

Open layouts joining kitchen, dining, and living spaces

Multiple bedrooms and bathrooms

Natural light and good room flow

Recent Upgrades

Smart improvements add real value. A basic kitchen update that costs $27,492 brings back $26,406 at sale—96.1% returned. Practical fixes work better than complete overhauls.

Outside improvements pay off, too. A new front door costs $2,355 but returns 188.1% at sale. A garage door replacement, at $4,513, brings back 193.9%. Fresh paint typically adds $10,184 to home value.

Market Conditions

Supply and demand drive property values. When fewer homes are for sale, prices rise as buyers compete. Lower interest rates usually bring more buyers to the market.

The broader economy also affects home values. Harvard's research shows that Americans plan to spend $509 billion fixing up homes in 2025. Homeowner equity grew 2.5% in late 2024, indicating the market's health.

Common Home Appraisal Problems

The home appraisal process can encounter some obstacles. Here are some things to watch for and how to handle these common issues.

Low Appraisal Value

Buyers and sellers face tough decisions when appraisals come in below the agreed purchase price. The appraiser might have used old data or missed recent sales in your area.

Watch out if you're near foreclosures or bank-owned properties. These distressed sales can lower the neighborhood's values. Buyers in declining markets might need to make more significant home down payments.

Property Condition Issues

The appraiser must note any problems affecting your home's safety and structure. Properties rated C6 show serious difficulties and won't qualify for regular loans until they are fixed. They look for:

Foundation damage or structural issues

Old HVAC systems needing replacement

Broken windows or missing handrails

Signs of pest problems

Roof troubles needing certification

Don't get stuck holding the bag on repairs - foundation work runs from $4,000 to $100,000 for full replacement. Homes rated C1 through C4 can still get loans, but C5 and C6 properties need repairs first.

Missing Documentation

Suitable paperwork makes all the difference. The appraiser needs to see and measure every part of your property. Missing documents can stall the process or lower your value.

Tell the appraiser about your improvements - skipping this step often means a lower value. Show receipts and photos of your upgrades to support a higher number.

Think your appraisal missed the mark? You can ask for a Reconsideration of Value (ROV). But you'll need proof - either overlooked improvements or comparable sales the appraiser didn't see. Keep those renovation records handy to back up your home's worth.

How to Prepare for Your Home Appraisal

A well-prepared home shows the appraiser that you care about maintenance. Taking time to get ready makes a real difference in your final value.

Clean and Declutter

The appraiser sees a clean, organized home as a sign of good maintenance. Take out anything that makes rooms look smaller or blocks important areas. A thorough cleaning lets the appraiser see your home's condition without distractions.

Start with these spots:

Deep clean those carpet stains

Touch up paint where needed

Make sure we can get to attics and crawl spaces

Power wash the outside

Clean up the yard and landscaping

Gather Important Documents

The appraiser needs good records to value your property right. Create a detailed list of recent improvements with dates and costs. Pull together these papers after you schedule the appraisal:

Old appraisal reports

Property tax papers

Renovation permits

Recent home inspections

Records of major upgrades

Fix Minor Issues

Don't let minor problems hurt your value. The appraiser uses the "$500 rule" - valuing homes in $500 steps. Small repairs can add significant value when you fix several things.

Take care of these typical troubles:

Fix those leaky faucets

Patch damaged walls and paint

Replace broken door handles

Tighten loose handrails

Check all mechanical systems

Make sure safety equipment works, too. Test carbon monoxide detectors, smoke alarms, and garage door openers. Fixing these items shows you take care of the property.

The outside counts just as much. Trim those bushes, mow the lawn, and clear out dead plants. Add some flowers in warm months, or keep snow cleared in winter.

Tell the appraiser about neighborhood improvements, too. New schools, parks, or better roads can boost your property's value. Your local knowledge helps you get the most accurate number for your property.

Conclusion

The home appraisal protects both you and your lender. Understanding and preparing for the process can help you secure your property's actual value.

The property condition tells the story. Clean, well-kept homes with good improvement records bring better numbers. A little effort in fixing minor problems and organizing paperwork before the appraiser arrives makes a real difference.

Banks Valuation takes great pride in offering accurate, fair valuations based on current market conditions and neighborhood factors. We understand how location and market trends shape your property's worth.

Trust us to guide you through the appraisal process. We handle any issues quickly and communicate openly with all parties. Our team of expert appraisers delivers the attention to detail, proper preparation, and professional guidance your valuable investment deserves.

The home appraisal protects buyers and lenders from overpaying for a property. Most U.S. homeowners lack proper insurance coverage, making accurate property valuation crucial for protecting their investments.

Home appraisals typically cost $300 to $450, with prices reaching $700 in high-demand markets like California. The appraiser needs 30 minutes to several hours at your property, while the process takes about a week to complete. When appraisals come in below expected value, you'll

need to either renegotiate the price, make up the difference in cash, or walk away from the deal.

This guide walks you through the appraisal process step by step. You'll learn what happens during a property inspection, what drives the cost, and how to prepare your home. We explain the key factors affecting your property's value and help you spot potential problems before they arise.

What Happens During a Home Appraisal

"The 2025 UAD overhaul introduces a flexible, customizable format for appraisals. Unlike the traditional, static forms, the new UAD 3.6 system tailors each report to match the property specifics, including only the necessary data fields." — Capital Valuations VA, Real Estate Valuation Company

Depending on the home's size and layout, the assigned appraiser views and measures your property during an on-site visit between 30 minutes and a few hours.

The Initial Property Walkthrough

The appraiser starts by walking through your entire home. They count bedrooms and bathrooms while assessing the floor plan's functionality. Both interior and exterior features are carefully examined to understand your home's essential characteristics.

Taking Measurements and Photos

The appraiser documents every aspect of your property. They take detailed photographs and create an exterior sketch of the building. The final report must include:

Maps showing the property location

Exterior photos - front and back views

Pictures of comparable properties used

Complete property layout documentation

Photos of each room

Checking Home Condition

The appraiser examines your home's key components. They assess the foundation, roof condition, walls, and structural elements.

During this inspection, they check all significant systems, such as HVAC and plumbing. Your home's features and recent improvements get special attention since these affect the final value. The appraiser notes any issues needing repair or safety concerns that might lower the property value.

The inspection goes beyond the main living spaces. The appraiser examines attics, basements, and crawl spaces to verify safety standards and assess their contribution to home value. Outside areas like landscaping, decks, and other improvements are also factors in the final assessment.

Home Appraisal Costs for 2025

The cost of the home appraisal is traditionally the buyer's responsibility. Most homeowners pay around $357, with the national average for a single-family home appraisal falling between $314 and $423.

What Affects the Cost

Square footage plays a significant role in your appraisal fee. Larger homes need more time to evaluate, which increases the cost. Properties in high-cost areas often start at $600.

Different loan types require different levels of detail. Here's what you'll pay for government-backed loans:

FHA appraisals: $400 to $700

VA appraisals: $425 to $900

Property condition and access also matter. Well-maintained homes with easy access stay within standard price ranges. However, homes with structural problems or hard-to-reach areas might cost over $1,000 for a basic assessment.

Market activity in your area affects pricing. The high demand for appraisers drives up costs. Rural properties and unique homes require more research time, leading to higher fees.

Key Factors That Impact Your Home's Value

"Homes with more usable space generally appraise higher, so any functional improvements or optimizations can be a plus." — Better Mortgage, Digital Mortgage Lender

The appraiser looks at several key elements when determining your property's worth. These factors work together to give us your home's actual market value.

Location and Neighborhood

Location remains the ever-popular "location, location, location" factor in property value. Homes near quality schools, shopping centers, and public transportation attract higher prices, and buyers are more interested in properties in safe neighborhoods with good school districts.

Future neighborhood prospects matter, too. New roads, shopping centers, and other developments boost property values, and job growth in the area often means rising home prices.

Property Size and Layout

Square footage tells part of the story. A 2,000-square-foot house selling for $200,000 is priced at $100 per square foot. But usable space matters more than raw numbers. We don't count garages, attics, or unfinished basements in the living space calculations.

The floor plan's function weighs heavily in our assessment. Homes get better valuations with:

Open layouts joining kitchen, dining, and living spaces

Multiple bedrooms and bathrooms

Natural light and good room flow

Recent Upgrades

Smart improvements add real value. A basic kitchen update that costs $27,492 brings back $26,406 at sale—96.1% returned. Practical fixes work better than complete overhauls.

Outside improvements pay off, too. A new front door costs $2,355 but returns 188.1% at sale. A garage door replacement, at $4,513, brings back 193.9%. Fresh paint typically adds $10,184 to home value.

Market Conditions

Supply and demand drive property values. When fewer homes are for sale, prices rise as buyers compete. Lower interest rates usually bring more buyers to the market.

The broader economy also affects home values. Harvard's research shows that Americans plan to spend $509 billion fixing up homes in 2025. Homeowner equity grew 2.5% in late 2024, indicating the market's health.

Common Home Appraisal Problems

The home appraisal process can encounter some obstacles. Here are some things to watch for and how to handle these common issues.

Low Appraisal Value

Buyers and sellers face tough decisions when appraisals come in below the agreed purchase price. The appraiser might have used old data or missed recent sales in your area.

Watch out if you're near foreclosures or bank-owned properties. These distressed sales can lower the neighborhood's values. Buyers in declining markets might need to make more significant home down payments.

Property Condition Issues

The appraiser must note any problems affecting your home's safety and structure. Properties rated C6 show serious difficulties and won't qualify for regular loans until they are fixed. They look for:

Foundation damage or structural issues

Old HVAC systems needing replacement

Broken windows or missing handrails

Signs of pest problems

Roof troubles needing certification

Don't get stuck holding the bag on repairs - foundation work runs from $4,000 to $100,000 for full replacement. Homes rated C1 through C4 can still get loans, but C5 and C6 properties need repairs first.

Missing Documentation

Suitable paperwork makes all the difference. The appraiser needs to see and measure every part of your property. Missing documents can stall the process or lower your value.

Tell the appraiser about your improvements - skipping this step often means a lower value. Show receipts and photos of your upgrades to support a higher number.

Think your appraisal missed the mark? You can ask for a Reconsideration of Value (ROV). But you'll need proof - either overlooked improvements or comparable sales the appraiser didn't see. Keep those renovation records handy to back up your home's worth.

How to Prepare for Your Home Appraisal

A well-prepared home shows the appraiser that you care about maintenance. Taking time to get ready makes a real difference in your final value.

Clean and Declutter

The appraiser sees a clean, organized home as a sign of good maintenance. Take out anything that makes rooms look smaller or blocks important areas. A thorough cleaning lets the appraiser see your home's condition without distractions.

Start with these spots:

Deep clean those carpet stains

Touch up paint where needed

Make sure we can get to attics and crawl spaces

Power wash the outside

Clean up the yard and landscaping

Gather Important Documents

The appraiser needs good records to value your property right. Create a detailed list of recent improvements with dates and costs. Pull together these papers after you schedule the appraisal:

Old appraisal reports

Property tax papers

Renovation permits

Recent home inspections

Records of major upgrades

Fix Minor Issues

Don't let minor problems hurt your value. The appraiser uses the "$500 rule" - valuing homes in $500 steps. Small repairs can add significant value when you fix several things.

Take care of these typical troubles:

Fix those leaky faucets

Patch damaged walls and paint

Replace broken door handles

Tighten loose handrails

Check all mechanical systems

Make sure safety equipment works, too. Test carbon monoxide detectors, smoke alarms, and garage door openers. Fixing these items shows you take care of the property.

The outside counts just as much. Trim those bushes, mow the lawn, and clear out dead plants. Add some flowers in warm months, or keep snow cleared in winter.

Tell the appraiser about neighborhood improvements, too. New schools, parks, or better roads can boost your property's value. Your local knowledge helps you get the most accurate number for your property.

Conclusion

The home appraisal protects both you and your lender. Understanding and preparing for the process can help you secure your property's actual value.

The property condition tells the story. Clean, well-kept homes with good improvement records bring better numbers. A little effort in fixing minor problems and organizing paperwork before the appraiser arrives makes a real difference.

Banks Valuation takes great pride in offering accurate, fair valuations based on current market conditions and neighborhood factors. We understand how location and market trends shape your property's worth.

Trust us to guide you through the appraisal process. We handle any issues quickly and communicate openly with all parties. Our team of expert appraisers delivers the attention to detail, proper preparation, and professional guidance your valuable investment deserves.

The home appraisal protects buyers and lenders from overpaying for a property. Most U.S. homeowners lack proper insurance coverage, making accurate property valuation crucial for protecting their investments.

Home appraisals typically cost $300 to $450, with prices reaching $700 in high-demand markets like California. The appraiser needs 30 minutes to several hours at your property, while the process takes about a week to complete. When appraisals come in below expected value, you'll

need to either renegotiate the price, make up the difference in cash, or walk away from the deal.

This guide walks you through the appraisal process step by step. You'll learn what happens during a property inspection, what drives the cost, and how to prepare your home. We explain the key factors affecting your property's value and help you spot potential problems before they arise.

What Happens During a Home Appraisal

"The 2025 UAD overhaul introduces a flexible, customizable format for appraisals. Unlike the traditional, static forms, the new UAD 3.6 system tailors each report to match the property specifics, including only the necessary data fields." — Capital Valuations VA, Real Estate Valuation Company

Depending on the home's size and layout, the assigned appraiser views and measures your property during an on-site visit between 30 minutes and a few hours.

The Initial Property Walkthrough

The appraiser starts by walking through your entire home. They count bedrooms and bathrooms while assessing the floor plan's functionality. Both interior and exterior features are carefully examined to understand your home's essential characteristics.

Taking Measurements and Photos

The appraiser documents every aspect of your property. They take detailed photographs and create an exterior sketch of the building. The final report must include:

Maps showing the property location

Exterior photos - front and back views

Pictures of comparable properties used

Complete property layout documentation

Photos of each room

Checking Home Condition

The appraiser examines your home's key components. They assess the foundation, roof condition, walls, and structural elements.

During this inspection, they check all significant systems, such as HVAC and plumbing. Your home's features and recent improvements get special attention since these affect the final value. The appraiser notes any issues needing repair or safety concerns that might lower the property value.

The inspection goes beyond the main living spaces. The appraiser examines attics, basements, and crawl spaces to verify safety standards and assess their contribution to home value. Outside areas like landscaping, decks, and other improvements are also factors in the final assessment.

Home Appraisal Costs for 2025

The cost of the home appraisal is traditionally the buyer's responsibility. Most homeowners pay around $357, with the national average for a single-family home appraisal falling between $314 and $423.

What Affects the Cost

Square footage plays a significant role in your appraisal fee. Larger homes need more time to evaluate, which increases the cost. Properties in high-cost areas often start at $600.

Different loan types require different levels of detail. Here's what you'll pay for government-backed loans:

FHA appraisals: $400 to $700

VA appraisals: $425 to $900

Property condition and access also matter. Well-maintained homes with easy access stay within standard price ranges. However, homes with structural problems or hard-to-reach areas might cost over $1,000 for a basic assessment.

Market activity in your area affects pricing. The high demand for appraisers drives up costs. Rural properties and unique homes require more research time, leading to higher fees.

Key Factors That Impact Your Home's Value

"Homes with more usable space generally appraise higher, so any functional improvements or optimizations can be a plus." — Better Mortgage, Digital Mortgage Lender

The appraiser looks at several key elements when determining your property's worth. These factors work together to give us your home's actual market value.

Location and Neighborhood

Location remains the ever-popular "location, location, location" factor in property value. Homes near quality schools, shopping centers, and public transportation attract higher prices, and buyers are more interested in properties in safe neighborhoods with good school districts.

Future neighborhood prospects matter, too. New roads, shopping centers, and other developments boost property values, and job growth in the area often means rising home prices.

Property Size and Layout

Square footage tells part of the story. A 2,000-square-foot house selling for $200,000 is priced at $100 per square foot. But usable space matters more than raw numbers. We don't count garages, attics, or unfinished basements in the living space calculations.

The floor plan's function weighs heavily in our assessment. Homes get better valuations with:

Open layouts joining kitchen, dining, and living spaces

Multiple bedrooms and bathrooms

Natural light and good room flow

Recent Upgrades

Smart improvements add real value. A basic kitchen update that costs $27,492 brings back $26,406 at sale—96.1% returned. Practical fixes work better than complete overhauls.

Outside improvements pay off, too. A new front door costs $2,355 but returns 188.1% at sale. A garage door replacement, at $4,513, brings back 193.9%. Fresh paint typically adds $10,184 to home value.

Market Conditions

Supply and demand drive property values. When fewer homes are for sale, prices rise as buyers compete. Lower interest rates usually bring more buyers to the market.

The broader economy also affects home values. Harvard's research shows that Americans plan to spend $509 billion fixing up homes in 2025. Homeowner equity grew 2.5% in late 2024, indicating the market's health.

Common Home Appraisal Problems

The home appraisal process can encounter some obstacles. Here are some things to watch for and how to handle these common issues.

Low Appraisal Value

Buyers and sellers face tough decisions when appraisals come in below the agreed purchase price. The appraiser might have used old data or missed recent sales in your area.

Watch out if you're near foreclosures or bank-owned properties. These distressed sales can lower the neighborhood's values. Buyers in declining markets might need to make more significant home down payments.

Property Condition Issues

The appraiser must note any problems affecting your home's safety and structure. Properties rated C6 show serious difficulties and won't qualify for regular loans until they are fixed. They look for:

Foundation damage or structural issues

Old HVAC systems needing replacement

Broken windows or missing handrails

Signs of pest problems

Roof troubles needing certification

Don't get stuck holding the bag on repairs - foundation work runs from $4,000 to $100,000 for full replacement. Homes rated C1 through C4 can still get loans, but C5 and C6 properties need repairs first.

Missing Documentation

Suitable paperwork makes all the difference. The appraiser needs to see and measure every part of your property. Missing documents can stall the process or lower your value.

Tell the appraiser about your improvements - skipping this step often means a lower value. Show receipts and photos of your upgrades to support a higher number.

Think your appraisal missed the mark? You can ask for a Reconsideration of Value (ROV). But you'll need proof - either overlooked improvements or comparable sales the appraiser didn't see. Keep those renovation records handy to back up your home's worth.

How to Prepare for Your Home Appraisal

A well-prepared home shows the appraiser that you care about maintenance. Taking time to get ready makes a real difference in your final value.

Clean and Declutter

The appraiser sees a clean, organized home as a sign of good maintenance. Take out anything that makes rooms look smaller or blocks important areas. A thorough cleaning lets the appraiser see your home's condition without distractions.

Start with these spots:

Deep clean those carpet stains

Touch up paint where needed

Make sure we can get to attics and crawl spaces

Power wash the outside

Clean up the yard and landscaping

Gather Important Documents

The appraiser needs good records to value your property right. Create a detailed list of recent improvements with dates and costs. Pull together these papers after you schedule the appraisal:

Old appraisal reports

Property tax papers

Renovation permits

Recent home inspections

Records of major upgrades

Fix Minor Issues

Don't let minor problems hurt your value. The appraiser uses the "$500 rule" - valuing homes in $500 steps. Small repairs can add significant value when you fix several things.

Take care of these typical troubles:

Fix those leaky faucets

Patch damaged walls and paint

Replace broken door handles

Tighten loose handrails

Check all mechanical systems

Make sure safety equipment works, too. Test carbon monoxide detectors, smoke alarms, and garage door openers. Fixing these items shows you take care of the property.

The outside counts just as much. Trim those bushes, mow the lawn, and clear out dead plants. Add some flowers in warm months, or keep snow cleared in winter.

Tell the appraiser about neighborhood improvements, too. New schools, parks, or better roads can boost your property's value. Your local knowledge helps you get the most accurate number for your property.

Conclusion

The home appraisal protects both you and your lender. Understanding and preparing for the process can help you secure your property's actual value.

The property condition tells the story. Clean, well-kept homes with good improvement records bring better numbers. A little effort in fixing minor problems and organizing paperwork before the appraiser arrives makes a real difference.

Banks Valuation takes great pride in offering accurate, fair valuations based on current market conditions and neighborhood factors. We understand how location and market trends shape your property's worth.

Trust us to guide you through the appraisal process. We handle any issues quickly and communicate openly with all parties. Our team of expert appraisers delivers the attention to detail, proper preparation, and professional guidance your valuable investment deserves.

02/04/2025

How to Secure an Appraisal to Remove PMI

From minimalist chic to bohemian flair, we'll delve into a myriad of design styles

02/04/2025

How to Secure an Appraisal to Remove PMI

From minimalist chic to bohemian flair, we'll delve into a myriad of design styles

02/04/2025

How to Secure an Appraisal to Remove PMI

From minimalist chic to bohemian flair, we'll delve into a myriad of design styles

02/04/2025

How to Secure an Appraisal to Remove PMI

From minimalist chic to bohemian flair, we'll delve into a myriad of design styles

01/21/2025

Home Appraisal Timeline and Process Guide for 2025

From minimalist chic to bohemian flair, we'll delve into a myriad of design styles

01/21/2025

Home Appraisal Timeline and Process Guide for 2025

From minimalist chic to bohemian flair, we'll delve into a myriad of design styles

01/21/2025

Home Appraisal Timeline and Process Guide for 2025

From minimalist chic to bohemian flair, we'll delve into a myriad of design styles

01/21/2025

Home Appraisal Timeline and Process Guide for 2025

From minimalist chic to bohemian flair, we'll delve into a myriad of design styles