Posted on

04/01/2025

FHA vs Conventional Appraisal: Key Differences Homebuyers Must Know

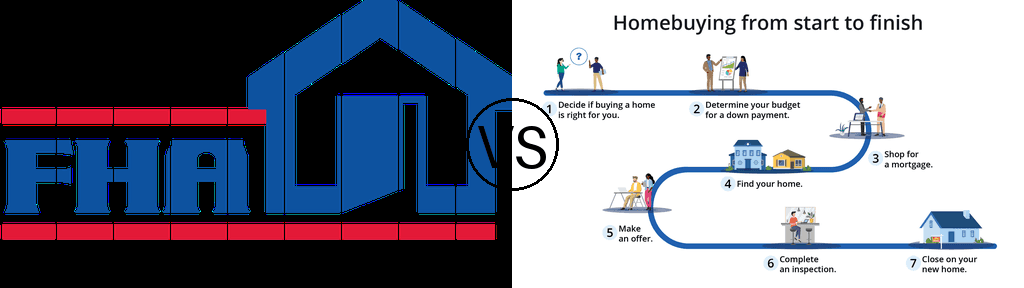

To buy a home with a mortgage, you need to know the key differences between an FHA and conventional appraisal. Most mortgage lenders require an appraisal to check a property's value before they approve your loan.

These two types of appraisals serve different purposes. FHA appraisals are designed for FHA loans. They emphasize safety and security standards set by the U.S. Department of Housing and Urban Development. Conventional appraisals mainly look at the property's value and condition.

The FHA loan option lets you make a lower down payment, making it a popular choice for first-time homebuyers. The appraisal process will give you a complete picture of the property. It has detailed inspections of attics and crawl spaces. The inspector will even check for peeling paint in homes built before 1978.

Learning these differences as you start your home-buying trip can save you time and help you avoid surprises. Let's examine what makes these appraisals different and help you find which option better suits your needs.

Understanding FHA and Conventional Appraisals

What is an FHA Appraisal?

An FHA appraisal is a detailed evaluation performed by an FHA-approved professional to determine the property's value and whether it meets safety standards. We check everything from the foundation to the roof, ensuring the home meets the U.S. Department of Housing and Urban Development's minimum property requirements.

What is a Conventional Appraisal?

Conventional appraisals mainly assess a property's market value. They are nowhere near as strict as FHA appraisals, which examine the property's condition and similar sales in the area. Buyers and sellers have more room to negotiate repairs with conventional appraisals.

Why Appraisals Matter for Homebuyers

Appraisals protect you and your lender's investment. The lender must know they're not lending more than the property's worth. On top of that, it helps you avoid paying too much for a house.

Here's what makes appraisals a vital part of buying a home:

They show the fair market value based on location, features, and recent sales

Your loan terms and down payment requirements depend on them

They can shape your property tax assessments and future refinancing options

The appraisal results can substantially affect your mortgage approval. If the appraisal is lower than expected, you should renegotiate the price or put more money down.

Key Property Requirements

Property standards are the foundations of both FHA and conventional appraisals. Each type has its requirements for approval.

FHA Property Standards

FHA property standards focus on three core aspects: safety, security, and structural soundness. According to the U.S. Department of Housing and Urban Development, properties must have proper drainage, functional utilities, and a roof with at least two years of remaining life. The requirements also call for strong foundations without cracks, not severely damaged walls, and good ventilation in attics and crawl spaces.

Conventional Property Standards

A rating system from C1 to C6 measures a property's condition in standard appraisals. Properties need to be residential and available by roads for year-round use. The property's utility connections should meet community standards.

Common Deal-Breakers in Both Types

Both FHA and conventional appraisals can fail due to these issues:

Structural problems that affect safety or integrity

Active pest infestations and extensive water damage

Environmental hazards and soil contamination

Building code violations

Both types of appraisals want to protect buyers and lenders. FHA standards tend to be stricter about safety and habitability requirements. Understanding these requirements helps you get ready for challenges in the appraisal process.

Appraisal Process Timeline

The completion timeline differs between FHA and conventional loan appraisals. Each type follows its process and takes a specific amount of time.

FHA Appraisal Steps and Duration

The FHA appraisal process starts 48 hours after the seller accepts your offer. Depending on the property's size and complexity, a physical inspection takes 30 minutes to several hours. Appraisers need 6-20 days to complete their reports.

Your FHA appraisal stays valid for 120 days, and you might get a 30-day extension in some cases. You'll need a new appraisal if you go beyond this timeframe. The original appraiser must check any required repairs and update the property value.

Conventional Appraisal Timeline

Conventional appraisals have different validity periods. New homes are suitable for up to 12 months, while other home appraisals last about four months.

Key timeline points for conventional appraisals include:

Appraisers schedule visits within 48 hours after order

Property inspection takes 30 minutes to several hours

Reports take 6-20 days to complete

Several factors can extend this timeline. Property complexity, market conditions, and the appraiser's workload all play a role. One example is that unique properties take longer. Appraisers need time to find comparable sales data. FHA and conventional appraisals are wrapped up in the usual 30-60-day mortgage closing window.

Cost Comparison and Value

Knowing how much different appraisals cost helps you plan your home purchase budget better. Let's understand what you'll pay for FHA and conventional appraisals.

FHA Appraisal Costs

FHA appraisals typically range from USD 400.00 to USD 700.00. The price changes based on your property's size and location. Some cases cost you up to $900.00. You'll pay more because of stricter rules and extra inspection needs. Your lender usually pays the appraiser first, but you'll cover this cost when you close.

Conventional Appraisal Fees

The good news is conventional appraisals cost less, usually between $300.00 and $400.00. A 2023 National Association of Realtors survey shows the typical price is $500.00. Your final cost depends on your property's complexity and current market conditions.

Additional Expenses to Think About

The simple appraisal fee isn't all you need to budget for. Appraisal Management Companies (AMCs) often work as middlemen and can take up to 50% of the total appraisal fee. Properties that need multiple visits or extra research cost more.

Your final costs depend on:

Your property's size and complexity

Local market conditions

Required compliance inspections

Where your property is located

How easy it is to access your property

Rural or unique properties usually cost more to appraise. This is because finding similar sales data is tougher. Appraisers may charge more for mileage and time on complex evaluations.

FHA vs Conventional Appraisal

The home-buying experience becomes more apparent when you know the differences between FHA and conventional appraisals. FHA appraisals need stricter safety standards and complete inspections. Conventional appraisals focus primarily on assessing market value.

Your choice will depend on costs too. FHA appraisals cost between $400 and $700. Conventional appraisals are cheaper at $300 to $500. On top of that, these options have different validity periods. FHA appraisals last 120 days, while conventional appraisals on new builds can stay valid for up to 12 months.

Your specific needs and circumstances will guide your decision. First-time homebuyers often choose FHA appraisals. These detailed inspections are worth the extra cost as they provide more protection. Experienced buyers tend to prefer conventional appraisals for their efficient process and flexibility.

Banks Valuations' experienced professionals will give you accurate property valuations that align with your loan type. Note that both types of appraisals are the foundations of protecting your investment. They help lenders make smart decisions about

To buy a home with a mortgage, you need to know the key differences between an FHA and conventional appraisal. Most mortgage lenders require an appraisal to check a property's value before they approve your loan.

These two types of appraisals serve different purposes. FHA appraisals are designed for FHA loans. They emphasize safety and security standards set by the U.S. Department of Housing and Urban Development. Conventional appraisals mainly look at the property's value and condition.

The FHA loan option lets you make a lower down payment, making it a popular choice for first-time homebuyers. The appraisal process will give you a complete picture of the property. It has detailed inspections of attics and crawl spaces. The inspector will even check for peeling paint in homes built before 1978.

Learning these differences as you start your home-buying trip can save you time and help you avoid surprises. Let's examine what makes these appraisals different and help you find which option better suits your needs.

Understanding FHA and Conventional Appraisals

What is an FHA Appraisal?

An FHA appraisal is a detailed evaluation performed by an FHA-approved professional to determine the property's value and whether it meets safety standards. We check everything from the foundation to the roof, ensuring the home meets the U.S. Department of Housing and Urban Development's minimum property requirements.

What is a Conventional Appraisal?

Conventional appraisals mainly assess a property's market value. They are nowhere near as strict as FHA appraisals, which examine the property's condition and similar sales in the area. Buyers and sellers have more room to negotiate repairs with conventional appraisals.

Why Appraisals Matter for Homebuyers

Appraisals protect you and your lender's investment. The lender must know they're not lending more than the property's worth. On top of that, it helps you avoid paying too much for a house.

Here's what makes appraisals a vital part of buying a home:

They show the fair market value based on location, features, and recent sales

Your loan terms and down payment requirements depend on them

They can shape your property tax assessments and future refinancing options

The appraisal results can substantially affect your mortgage approval. If the appraisal is lower than expected, you should renegotiate the price or put more money down.

Key Property Requirements

Property standards are the foundations of both FHA and conventional appraisals. Each type has its requirements for approval.

FHA Property Standards

FHA property standards focus on three core aspects: safety, security, and structural soundness. According to the U.S. Department of Housing and Urban Development, properties must have proper drainage, functional utilities, and a roof with at least two years of remaining life. The requirements also call for strong foundations without cracks, not severely damaged walls, and good ventilation in attics and crawl spaces.

Conventional Property Standards

A rating system from C1 to C6 measures a property's condition in standard appraisals. Properties need to be residential and available by roads for year-round use. The property's utility connections should meet community standards.

Common Deal-Breakers in Both Types

Both FHA and conventional appraisals can fail due to these issues:

Structural problems that affect safety or integrity

Active pest infestations and extensive water damage

Environmental hazards and soil contamination

Building code violations

Both types of appraisals want to protect buyers and lenders. FHA standards tend to be stricter about safety and habitability requirements. Understanding these requirements helps you get ready for challenges in the appraisal process.

Appraisal Process Timeline

The completion timeline differs between FHA and conventional loan appraisals. Each type follows its process and takes a specific amount of time.

FHA Appraisal Steps and Duration

The FHA appraisal process starts 48 hours after the seller accepts your offer. Depending on the property's size and complexity, a physical inspection takes 30 minutes to several hours. Appraisers need 6-20 days to complete their reports.

Your FHA appraisal stays valid for 120 days, and you might get a 30-day extension in some cases. You'll need a new appraisal if you go beyond this timeframe. The original appraiser must check any required repairs and update the property value.

Conventional Appraisal Timeline

Conventional appraisals have different validity periods. New homes are suitable for up to 12 months, while other home appraisals last about four months.

Key timeline points for conventional appraisals include:

Appraisers schedule visits within 48 hours after order

Property inspection takes 30 minutes to several hours

Reports take 6-20 days to complete

Several factors can extend this timeline. Property complexity, market conditions, and the appraiser's workload all play a role. One example is that unique properties take longer. Appraisers need time to find comparable sales data. FHA and conventional appraisals are wrapped up in the usual 30-60-day mortgage closing window.

Cost Comparison and Value

Knowing how much different appraisals cost helps you plan your home purchase budget better. Let's understand what you'll pay for FHA and conventional appraisals.

FHA Appraisal Costs

FHA appraisals typically range from USD 400.00 to USD 700.00. The price changes based on your property's size and location. Some cases cost you up to $900.00. You'll pay more because of stricter rules and extra inspection needs. Your lender usually pays the appraiser first, but you'll cover this cost when you close.

Conventional Appraisal Fees

The good news is conventional appraisals cost less, usually between $300.00 and $400.00. A 2023 National Association of Realtors survey shows the typical price is $500.00. Your final cost depends on your property's complexity and current market conditions.

Additional Expenses to Think About

The simple appraisal fee isn't all you need to budget for. Appraisal Management Companies (AMCs) often work as middlemen and can take up to 50% of the total appraisal fee. Properties that need multiple visits or extra research cost more.

Your final costs depend on:

Your property's size and complexity

Local market conditions

Required compliance inspections

Where your property is located

How easy it is to access your property

Rural or unique properties usually cost more to appraise. This is because finding similar sales data is tougher. Appraisers may charge more for mileage and time on complex evaluations.

FHA vs Conventional Appraisal

The home-buying experience becomes more apparent when you know the differences between FHA and conventional appraisals. FHA appraisals need stricter safety standards and complete inspections. Conventional appraisals focus primarily on assessing market value.

Your choice will depend on costs too. FHA appraisals cost between $400 and $700. Conventional appraisals are cheaper at $300 to $500. On top of that, these options have different validity periods. FHA appraisals last 120 days, while conventional appraisals on new builds can stay valid for up to 12 months.

Your specific needs and circumstances will guide your decision. First-time homebuyers often choose FHA appraisals. These detailed inspections are worth the extra cost as they provide more protection. Experienced buyers tend to prefer conventional appraisals for their efficient process and flexibility.

Banks Valuations' experienced professionals will give you accurate property valuations that align with your loan type. Note that both types of appraisals are the foundations of protecting your investment. They help lenders make smart decisions about

To buy a home with a mortgage, you need to know the key differences between an FHA and conventional appraisal. Most mortgage lenders require an appraisal to check a property's value before they approve your loan.

These two types of appraisals serve different purposes. FHA appraisals are designed for FHA loans. They emphasize safety and security standards set by the U.S. Department of Housing and Urban Development. Conventional appraisals mainly look at the property's value and condition.

The FHA loan option lets you make a lower down payment, making it a popular choice for first-time homebuyers. The appraisal process will give you a complete picture of the property. It has detailed inspections of attics and crawl spaces. The inspector will even check for peeling paint in homes built before 1978.

Learning these differences as you start your home-buying trip can save you time and help you avoid surprises. Let's examine what makes these appraisals different and help you find which option better suits your needs.

Understanding FHA and Conventional Appraisals

What is an FHA Appraisal?

An FHA appraisal is a detailed evaluation performed by an FHA-approved professional to determine the property's value and whether it meets safety standards. We check everything from the foundation to the roof, ensuring the home meets the U.S. Department of Housing and Urban Development's minimum property requirements.

What is a Conventional Appraisal?

Conventional appraisals mainly assess a property's market value. They are nowhere near as strict as FHA appraisals, which examine the property's condition and similar sales in the area. Buyers and sellers have more room to negotiate repairs with conventional appraisals.

Why Appraisals Matter for Homebuyers

Appraisals protect you and your lender's investment. The lender must know they're not lending more than the property's worth. On top of that, it helps you avoid paying too much for a house.

Here's what makes appraisals a vital part of buying a home:

They show the fair market value based on location, features, and recent sales

Your loan terms and down payment requirements depend on them

They can shape your property tax assessments and future refinancing options

The appraisal results can substantially affect your mortgage approval. If the appraisal is lower than expected, you should renegotiate the price or put more money down.

Key Property Requirements

Property standards are the foundations of both FHA and conventional appraisals. Each type has its requirements for approval.

FHA Property Standards

FHA property standards focus on three core aspects: safety, security, and structural soundness. According to the U.S. Department of Housing and Urban Development, properties must have proper drainage, functional utilities, and a roof with at least two years of remaining life. The requirements also call for strong foundations without cracks, not severely damaged walls, and good ventilation in attics and crawl spaces.

Conventional Property Standards

A rating system from C1 to C6 measures a property's condition in standard appraisals. Properties need to be residential and available by roads for year-round use. The property's utility connections should meet community standards.

Common Deal-Breakers in Both Types

Both FHA and conventional appraisals can fail due to these issues:

Structural problems that affect safety or integrity

Active pest infestations and extensive water damage

Environmental hazards and soil contamination

Building code violations

Both types of appraisals want to protect buyers and lenders. FHA standards tend to be stricter about safety and habitability requirements. Understanding these requirements helps you get ready for challenges in the appraisal process.

Appraisal Process Timeline

The completion timeline differs between FHA and conventional loan appraisals. Each type follows its process and takes a specific amount of time.

FHA Appraisal Steps and Duration

The FHA appraisal process starts 48 hours after the seller accepts your offer. Depending on the property's size and complexity, a physical inspection takes 30 minutes to several hours. Appraisers need 6-20 days to complete their reports.

Your FHA appraisal stays valid for 120 days, and you might get a 30-day extension in some cases. You'll need a new appraisal if you go beyond this timeframe. The original appraiser must check any required repairs and update the property value.

Conventional Appraisal Timeline

Conventional appraisals have different validity periods. New homes are suitable for up to 12 months, while other home appraisals last about four months.

Key timeline points for conventional appraisals include:

Appraisers schedule visits within 48 hours after order

Property inspection takes 30 minutes to several hours

Reports take 6-20 days to complete

Several factors can extend this timeline. Property complexity, market conditions, and the appraiser's workload all play a role. One example is that unique properties take longer. Appraisers need time to find comparable sales data. FHA and conventional appraisals are wrapped up in the usual 30-60-day mortgage closing window.

Cost Comparison and Value

Knowing how much different appraisals cost helps you plan your home purchase budget better. Let's understand what you'll pay for FHA and conventional appraisals.

FHA Appraisal Costs

FHA appraisals typically range from USD 400.00 to USD 700.00. The price changes based on your property's size and location. Some cases cost you up to $900.00. You'll pay more because of stricter rules and extra inspection needs. Your lender usually pays the appraiser first, but you'll cover this cost when you close.

Conventional Appraisal Fees

The good news is conventional appraisals cost less, usually between $300.00 and $400.00. A 2023 National Association of Realtors survey shows the typical price is $500.00. Your final cost depends on your property's complexity and current market conditions.

Additional Expenses to Think About

The simple appraisal fee isn't all you need to budget for. Appraisal Management Companies (AMCs) often work as middlemen and can take up to 50% of the total appraisal fee. Properties that need multiple visits or extra research cost more.

Your final costs depend on:

Your property's size and complexity

Local market conditions

Required compliance inspections

Where your property is located

How easy it is to access your property

Rural or unique properties usually cost more to appraise. This is because finding similar sales data is tougher. Appraisers may charge more for mileage and time on complex evaluations.

FHA vs Conventional Appraisal

The home-buying experience becomes more apparent when you know the differences between FHA and conventional appraisals. FHA appraisals need stricter safety standards and complete inspections. Conventional appraisals focus primarily on assessing market value.

Your choice will depend on costs too. FHA appraisals cost between $400 and $700. Conventional appraisals are cheaper at $300 to $500. On top of that, these options have different validity periods. FHA appraisals last 120 days, while conventional appraisals on new builds can stay valid for up to 12 months.

Your specific needs and circumstances will guide your decision. First-time homebuyers often choose FHA appraisals. These detailed inspections are worth the extra cost as they provide more protection. Experienced buyers tend to prefer conventional appraisals for their efficient process and flexibility.

Banks Valuations' experienced professionals will give you accurate property valuations that align with your loan type. Note that both types of appraisals are the foundations of protecting your investment. They help lenders make smart decisions about

To buy a home with a mortgage, you need to know the key differences between an FHA and conventional appraisal. Most mortgage lenders require an appraisal to check a property's value before they approve your loan.

These two types of appraisals serve different purposes. FHA appraisals are designed for FHA loans. They emphasize safety and security standards set by the U.S. Department of Housing and Urban Development. Conventional appraisals mainly look at the property's value and condition.

The FHA loan option lets you make a lower down payment, making it a popular choice for first-time homebuyers. The appraisal process will give you a complete picture of the property. It has detailed inspections of attics and crawl spaces. The inspector will even check for peeling paint in homes built before 1978.

Learning these differences as you start your home-buying trip can save you time and help you avoid surprises. Let's examine what makes these appraisals different and help you find which option better suits your needs.

Understanding FHA and Conventional Appraisals

What is an FHA Appraisal?

An FHA appraisal is a detailed evaluation performed by an FHA-approved professional to determine the property's value and whether it meets safety standards. We check everything from the foundation to the roof, ensuring the home meets the U.S. Department of Housing and Urban Development's minimum property requirements.

What is a Conventional Appraisal?

Conventional appraisals mainly assess a property's market value. They are nowhere near as strict as FHA appraisals, which examine the property's condition and similar sales in the area. Buyers and sellers have more room to negotiate repairs with conventional appraisals.

Why Appraisals Matter for Homebuyers

Appraisals protect you and your lender's investment. The lender must know they're not lending more than the property's worth. On top of that, it helps you avoid paying too much for a house.

Here's what makes appraisals a vital part of buying a home:

They show the fair market value based on location, features, and recent sales

Your loan terms and down payment requirements depend on them

They can shape your property tax assessments and future refinancing options

The appraisal results can substantially affect your mortgage approval. If the appraisal is lower than expected, you should renegotiate the price or put more money down.

Key Property Requirements

Property standards are the foundations of both FHA and conventional appraisals. Each type has its requirements for approval.

FHA Property Standards

FHA property standards focus on three core aspects: safety, security, and structural soundness. According to the U.S. Department of Housing and Urban Development, properties must have proper drainage, functional utilities, and a roof with at least two years of remaining life. The requirements also call for strong foundations without cracks, not severely damaged walls, and good ventilation in attics and crawl spaces.

Conventional Property Standards

A rating system from C1 to C6 measures a property's condition in standard appraisals. Properties need to be residential and available by roads for year-round use. The property's utility connections should meet community standards.

Common Deal-Breakers in Both Types

Both FHA and conventional appraisals can fail due to these issues:

Structural problems that affect safety or integrity

Active pest infestations and extensive water damage

Environmental hazards and soil contamination

Building code violations

Both types of appraisals want to protect buyers and lenders. FHA standards tend to be stricter about safety and habitability requirements. Understanding these requirements helps you get ready for challenges in the appraisal process.

Appraisal Process Timeline

The completion timeline differs between FHA and conventional loan appraisals. Each type follows its process and takes a specific amount of time.

FHA Appraisal Steps and Duration

The FHA appraisal process starts 48 hours after the seller accepts your offer. Depending on the property's size and complexity, a physical inspection takes 30 minutes to several hours. Appraisers need 6-20 days to complete their reports.

Your FHA appraisal stays valid for 120 days, and you might get a 30-day extension in some cases. You'll need a new appraisal if you go beyond this timeframe. The original appraiser must check any required repairs and update the property value.

Conventional Appraisal Timeline

Conventional appraisals have different validity periods. New homes are suitable for up to 12 months, while other home appraisals last about four months.

Key timeline points for conventional appraisals include:

Appraisers schedule visits within 48 hours after order

Property inspection takes 30 minutes to several hours

Reports take 6-20 days to complete

Several factors can extend this timeline. Property complexity, market conditions, and the appraiser's workload all play a role. One example is that unique properties take longer. Appraisers need time to find comparable sales data. FHA and conventional appraisals are wrapped up in the usual 30-60-day mortgage closing window.

Cost Comparison and Value

Knowing how much different appraisals cost helps you plan your home purchase budget better. Let's understand what you'll pay for FHA and conventional appraisals.

FHA Appraisal Costs

FHA appraisals typically range from USD 400.00 to USD 700.00. The price changes based on your property's size and location. Some cases cost you up to $900.00. You'll pay more because of stricter rules and extra inspection needs. Your lender usually pays the appraiser first, but you'll cover this cost when you close.

Conventional Appraisal Fees

The good news is conventional appraisals cost less, usually between $300.00 and $400.00. A 2023 National Association of Realtors survey shows the typical price is $500.00. Your final cost depends on your property's complexity and current market conditions.

Additional Expenses to Think About

The simple appraisal fee isn't all you need to budget for. Appraisal Management Companies (AMCs) often work as middlemen and can take up to 50% of the total appraisal fee. Properties that need multiple visits or extra research cost more.

Your final costs depend on:

Your property's size and complexity

Local market conditions

Required compliance inspections

Where your property is located

How easy it is to access your property

Rural or unique properties usually cost more to appraise. This is because finding similar sales data is tougher. Appraisers may charge more for mileage and time on complex evaluations.

FHA vs Conventional Appraisal

The home-buying experience becomes more apparent when you know the differences between FHA and conventional appraisals. FHA appraisals need stricter safety standards and complete inspections. Conventional appraisals focus primarily on assessing market value.

Your choice will depend on costs too. FHA appraisals cost between $400 and $700. Conventional appraisals are cheaper at $300 to $500. On top of that, these options have different validity periods. FHA appraisals last 120 days, while conventional appraisals on new builds can stay valid for up to 12 months.

Your specific needs and circumstances will guide your decision. First-time homebuyers often choose FHA appraisals. These detailed inspections are worth the extra cost as they provide more protection. Experienced buyers tend to prefer conventional appraisals for their efficient process and flexibility.

Banks Valuations' experienced professionals will give you accurate property valuations that align with your loan type. Note that both types of appraisals are the foundations of protecting your investment. They help lenders make smart decisions about

02/04/2025

How to Secure an Appraisal to Remove PMI

From minimalist chic to bohemian flair, we'll delve into a myriad of design styles

02/04/2025

How to Secure an Appraisal to Remove PMI

From minimalist chic to bohemian flair, we'll delve into a myriad of design styles

02/04/2025

How to Secure an Appraisal to Remove PMI

From minimalist chic to bohemian flair, we'll delve into a myriad of design styles

02/04/2025

How to Secure an Appraisal to Remove PMI

From minimalist chic to bohemian flair, we'll delve into a myriad of design styles

01/21/2025

Home Appraisal Timeline and Process Guide for 2025

From minimalist chic to bohemian flair, we'll delve into a myriad of design styles

01/21/2025

Home Appraisal Timeline and Process Guide for 2025

From minimalist chic to bohemian flair, we'll delve into a myriad of design styles

01/21/2025

Home Appraisal Timeline and Process Guide for 2025

From minimalist chic to bohemian flair, we'll delve into a myriad of design styles

01/21/2025

Home Appraisal Timeline and Process Guide for 2025

From minimalist chic to bohemian flair, we'll delve into a myriad of design styles